What you'll see in your inbox.

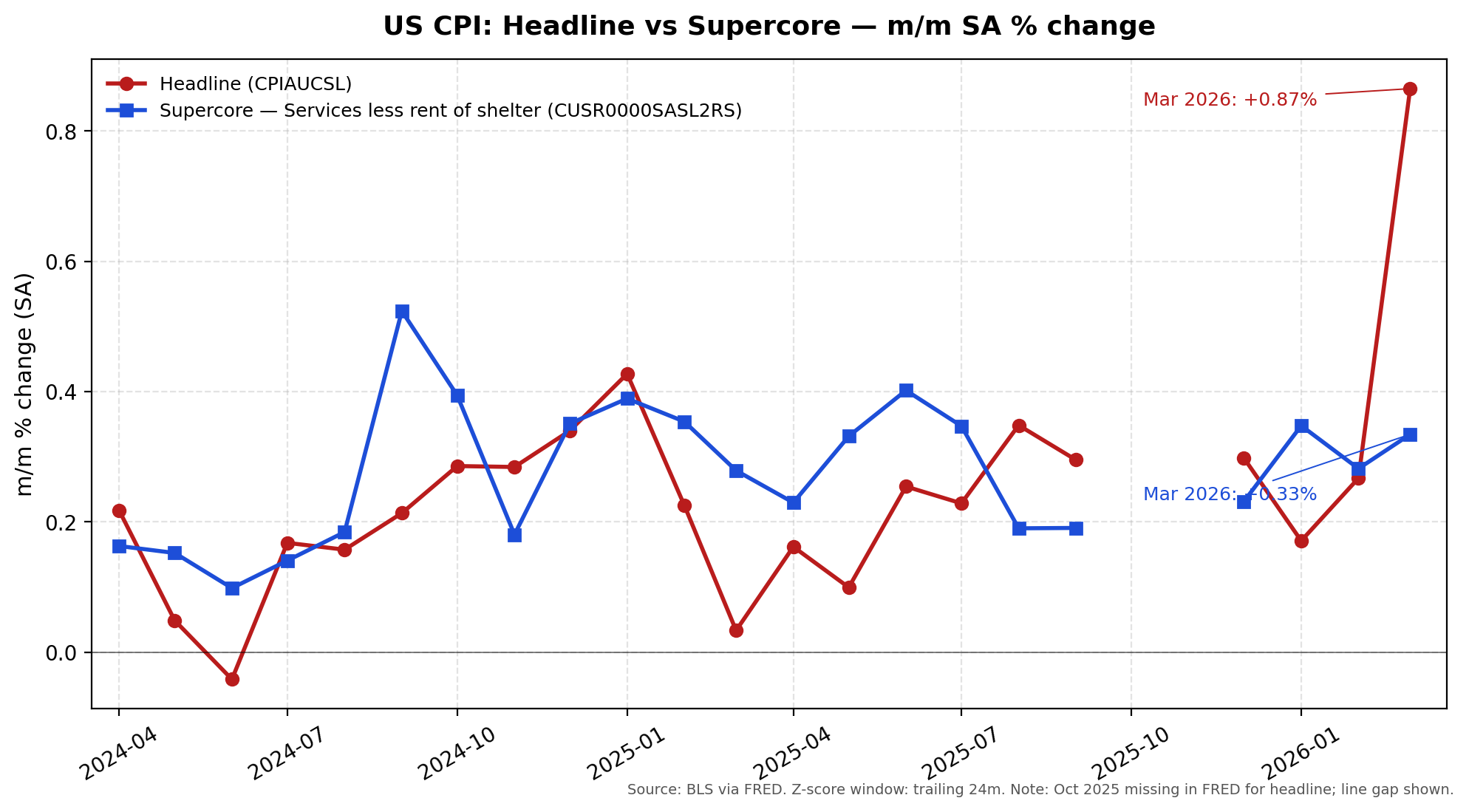

Headline vs. Supercore (services less rent of shelter), m/m SA — the divergence chart from the March 2026 release.

CUSR0000SA0, CUSR0000SASL2RS). Charted on April 10, 2026.

QuantVeritas turns each BLS release into a clean component decomposition, surprise z-scores, and the implied OIS curve shift — in your inbox within 5 minutes of 8:30 AM ET.

One email per release. No spam. Unsubscribe any time. By subscribing you agree to our privacy policy.

Headline broken into shelter, core services ex-shelter, core goods, energy, and food — weighted contributions, sticky vs. flexible flagged.

Each subcomponent's surprise scored against its trailing 24-month distribution. See instantly which line items are doing the work.

OIS curve at 8:29 vs. 8:35 ET. Repricing in basis points at each FOMC meeting through year-end. EFFR-SOFR basis cross-check separates Fed-path repricing from money-market plumbing. One chart, no terminal needed.

Headline vs. Supercore (services less rent of shelter), m/m SA — the divergence chart from the March 2026 release.

CUSR0000SA0, CUSR0000SASL2RS). Charted on April 10, 2026.

The full Macro Intelligence memo from the March 2026 CPI release — component decomposition, surprise z-scores, OIS reaction window, sector mapping, and conditional positioning bias. Reproduced unedited.

Read the sample memo →Every release produces both. Free posts publicly; premium lands in your inbox.

Posted to X within five minutes of 8:30 ET. Hard cap: 300 words.

Everything in the free tier, plus the trade-floor read. 800–1200 words.

Pricing for the premium tier will be announced at launch. Waitlist subscribers get early access and a launch-window discount.

I'm Terence Agbeyegbe, Professor of Economics at Hunter College, CUNY. Applied econometrician with 20+ years researching the methods most desks use to read inflation. QuantVeritas is the tool I always wished I had on release morning.